It’s always sunny in Brisbane

Originally appeared in Live wire markets

RAM Director, Funds Management Mike Nguyen says the sun is shining on Brisbane’s commercial office real estate sector and the time to make hay is now.

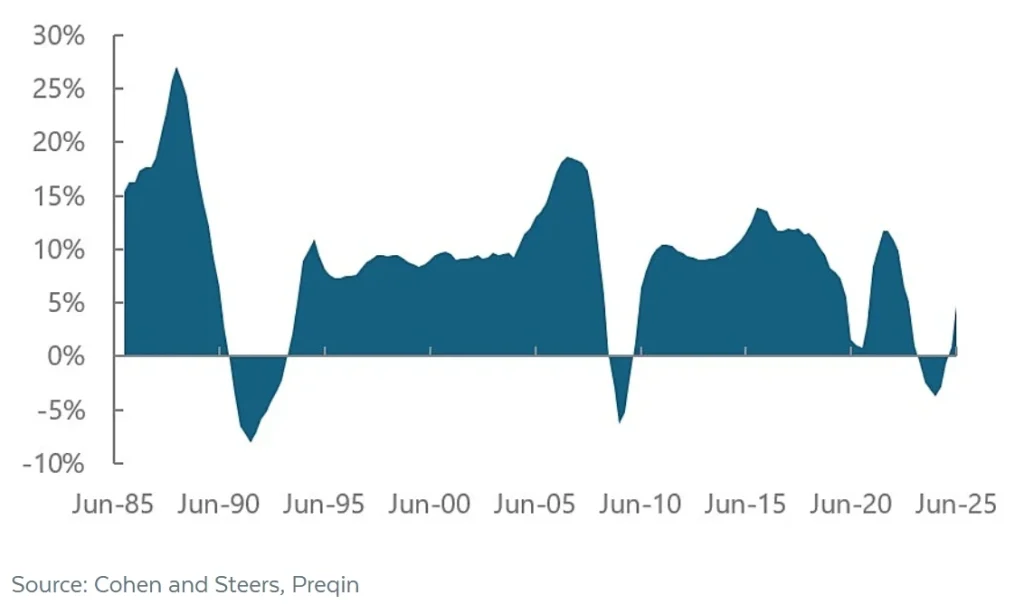

When it comes to commercial real estate investment, timing is everything. Historically, the best returns have been generated in the aftermath of market downturns – whether it’s the ‘recession we had to have’ in the early ‘90s, the GFC or more recently COVID.

Last year we saw green shoots start to emerge in Australian commercial real estate, with investment volumes rising 21% to around $30 billion, capitalisation rates stabilising and trending downwards, and office, retail and industrial outperforming.

Seasoned investors know there are no guarantees with market movements. But history suggests there could be an imminent uplift and opportunity to enter the market at a major discount, with the next 18 months potentially offering the best entry point into office assets since the GFC.

Historical Total Returns for Commercial Real Estate, 1985-2025

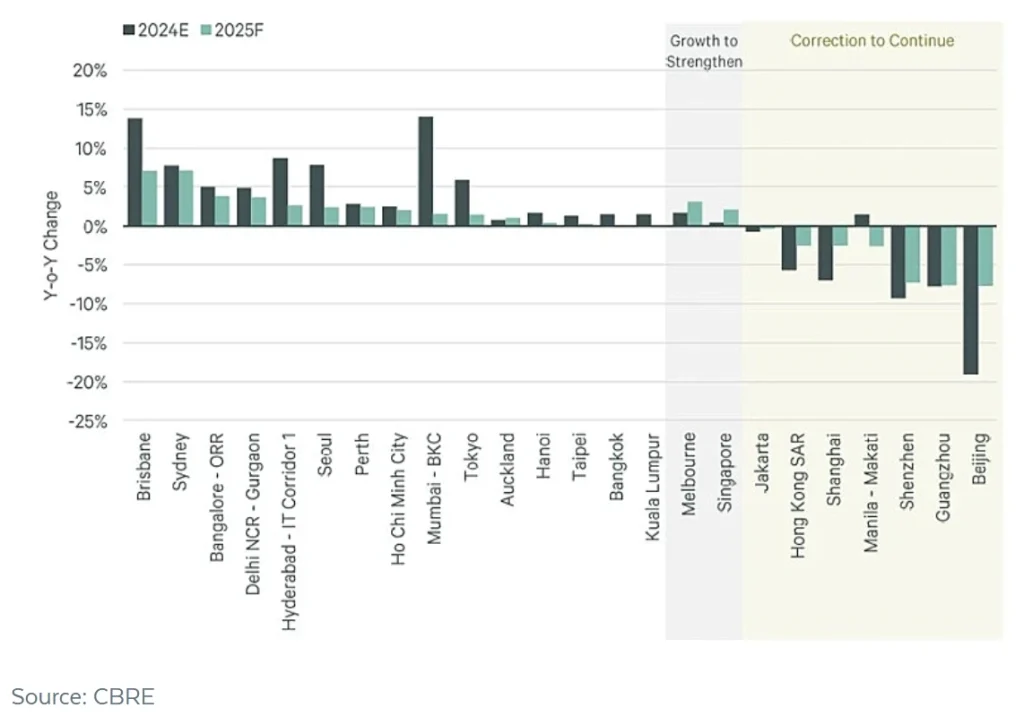

If we drill down into the state capital office market, we can see that Brisbane is at the head of the pack, recording its highest year-on-year effective rental growth in 2024 at 13.8%. While growth has moderated slightly since, continued tenant interest and a clear gap between new and existing stock are expected to support positive rental momentum.

More broadly, Brisbane is forecast to be the fastest-growing office market in the whole APAC region, outpacing even the fast-growing Indian megacities of Bangalore, Delhi and Hyderabad.

APAC Office Rentals, 2024-2025

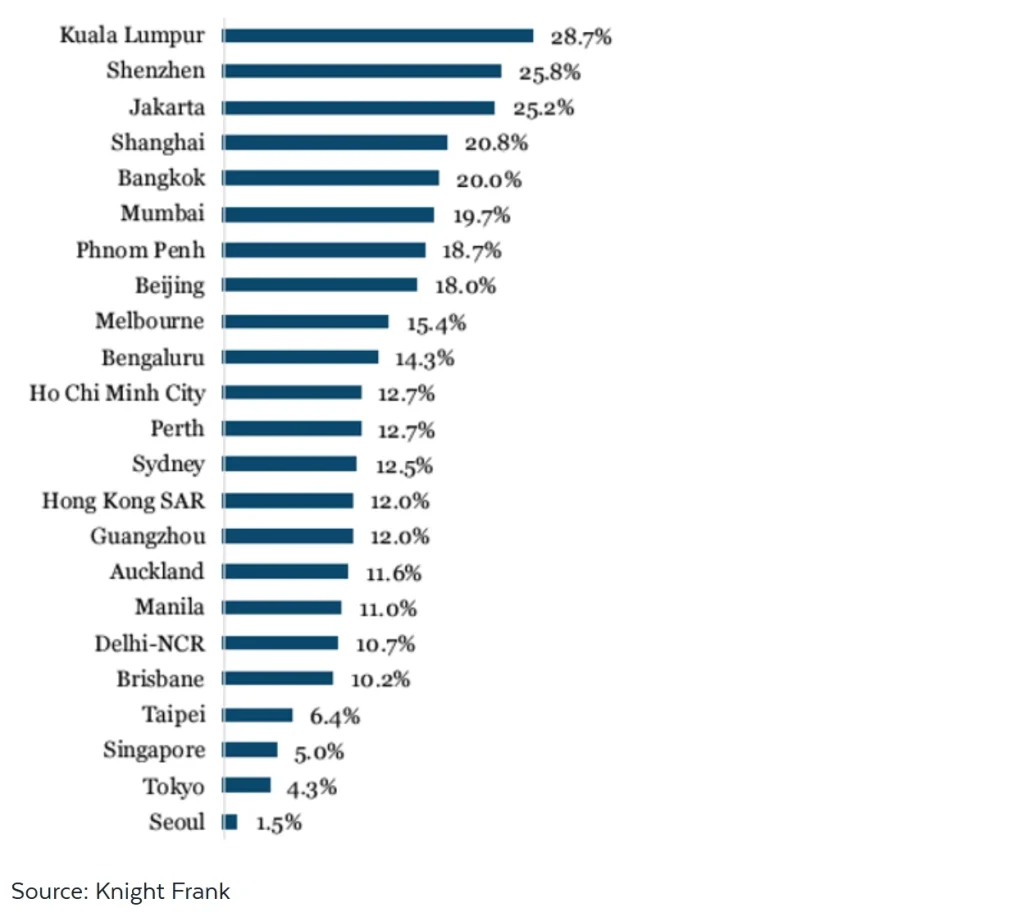

Total Brisbane CBD vacancy rates are at their lowest in a decade at around 10%, as well as being the lowest in Australia and the fifth lowest across the entire APAC region.

APAC Vacancy Rates, Q2 2024

Opportunity knocks

So why is Brisbane going gangbusters? One reason is simple geography. Unlike say Melbourne with its endless potential to expand and no official borders, Brisbane benefits from supply constraints due to the landlocked geography of the surrounding region, with a constrained catchment driven by the adjacent river, public transport networks, parkland and the CBD.

But more significantly, the dice are simply falling in favour of the Sunshine State. Brisbane’s office market is set to benefit from three macrotrends – demographic growth, working practices and sporting infrastructure.

1. All roads lead to the Sunshine State

Surging population growth is helping to deepen the workforce, expand tenant demand and support larger corporate footprints.

Queensland recorded an annual population growth rate of 2.0% in 2024, ahead of the national average of 1.8%, with strong interstate migration a crucial driver, driven by relative housing affordability.

ABS net interstate migration (NIM) data indicates Queensland is leading the way, with a net gain of 24,015 new Queenslanders in the year ending 31 March 2025[1].

Most of these migrants settle in the south-east. Brisbane is expected to experience the largest population growth among Australian capital cities over the next 10 years, with white-collar office employment outpacing global cities.

By 2040, Southeast Queensland is projected to accommodate an additional 1.9 million people, 800,000 new homes and 1 million new jobs – matching the current population of Greater Sydney.

Set to comprise 35.4% of the state’s workforce, the Brisbane region is projected to see up to a 12.7% increase in professional white-collar employment by 2025-26.

2. WFH is not here to stay

The post-COVID impact of working from home on the office sector has been well documented. But there are signs Australians are tiring of taking Zoom calls in their pyjamas, with WFH facing headwinds in 2024. Less than 10% of all job ads offered remote work and 87% of companies have started to implement mandatory office days.

It’s a mixed picture across the country, with Queensland employees and employers embracing the return to the CBD more readily than their southern counterparts. In terms of office attendance, Brisbane (88%) is second only to Perth (90%) with Sydney (76%) and Melbourne (61%) a fair way behind.

A combination of shifting employee sentiment and employer incentives mean projected daily attendance is projected to return to pre-pandemic levels.

This has helped vacancy levels fall to around 10% – the lowest in over a decade – with prime at 8.0% and secondary at 13%. Vacancies are expected to rise slightly this year before tightening post-2026.

3. The Olympics is an infrastructure catalyst

Brisbane is on track to host the 2032 Olympics, which is set to inject around $36 billion into the Queensland economy, boosting productivity, liveability and population growth.

A significant pipeline of key infrastructure projects is planned through to 2032, with a total expected cost of over $185 billion, with the Cross-River Rail project making commuting easier and driving office demand.

The value of scarcity

Higher demand from a growing population and workforce, coupled with constrained supply, will result in lower office vacancy and higher rental growth.

Crucially, new supply is limited compared with previous cycles due to rising development and labour costs.

Supply and pipeline remains stable for 2025 with 87,700sqm under construction (80% pre-committed) and no new major supply post-2026, supporting long-term rental growth.

Deep conviction

With Brisbane leading the national rebound and forecast to be the fastest-growing office market in the APAC region, it’s not surprising we have a deep conviction in Queensland commercial real estate at Real Asset Management (RAM).

And the numbers bear this out. In our listed and unlisted real estate funds, we have 14 assets in the Sunshine State, valued at around $600 million, as at 30 June 2025.

This includes 333 Ann Street, an A-grade trophy asset with strong tenant covenants, 99% occupancy and a 3.2-year weighted average lease expiry (WALE) in a gateway Brisbane CBD location.