RAM takes listed note structure into wholesale market

Originally appeared in Kanganews

RAM has raised A$90 million in the wholesale market using an OTC version of its ASX−listed secured income note structure. The reverse−enquiry led deal gives subsidiary Brighten Home Loans an additional funding channel, alongside warehousing, RMBS and unlisted credit funds.

The RAM Income Capital senior unrated notes rank pari passu with Real Asset Management (RAM)′s listed vehicle and are backed by the same residential mortgage portfolio, giving institutional investors exposure to the collateral at a pickup to comparable residential mortgage−backed securities (RMBS) mezzanine debt.

The transaction comes less than a year after RAM established an ASX−listed vehicle which raised A$300 million in the retail market, part of a wider trend of Australian asset managers using listed credit products to access retail and wealth investors. KangaNews reported after the October 2025 deal that demand for the listed notes had been supported by the demise of additional tier-one capital.

Michael Frearson, RAM’s executive director and Sydney-based head of fixed income, explains that the latest security is underpinned by the same portfolio as the RAM Secured Income Notes (RAMHA) and ranks pari-passu with the listed vehicle. “The only difference is that it is an OTC [over the counter] security for wholesale investors, allowing us to diversify the investor base,” he adds.

The deal highlights an evolution in RAM’s funding strategy for its wholly owned subsidiary Brighten, with the OTC and listed notes comprising its fourth pillar of financing. Warehousing, RMBS and unlisted credit funds are other sources of capital.

RAM says the OTC secured notes programme adds another channel that it intends to grow alongside its listed vehicle.

Demand exceeded expectations, allowing RAM to increase the transaction from an initial A$50 million target and tighten pricing by 10 basis points. The deal was supported by reverse enquiry from wholesale investors, including a cornerstone account that ultimately represented more than half the final book.

RAM had been confident of investor demand, due to the fixed-rate structure underlying asset quality, execution window and truncated deal process, Frearson explains.

“Domestic yields are close to six-year highs. Given strong demand and interest-rate volatility, investors preferred the certainty of a fixed-rate structure and wanted the rate locked in before rates moved. We therefore closed the book and priced the deal after only one day. Future OTC transactions will involve broader investor engagement as the programme expands,” he tells KangaNews.

Robert Moulton, executive director, DCM and syndicate at Westpac Institutional Bank in Brisbane, says the reverse enquiry originated from a “coupon-focused network” and so spread was not the primary performance metric.

Even so, sub-investment-grade tier-two securities provided a reference point for the bespoke trade, he adds.

He tells KangaNews: “The deal was all about the coupon. The interested investor network also had some timing requirements that we were working toward. We had to execute ahead of the Australian school holidays which led to an accelerated timetable that probably wasn’t the natural timeline for an inaugural OTC deal. As such, our target investor base was narrowed to those already familiar with the credit and structure from RAM’s ASX-listed issue.”

PROGRAMME GROWTH

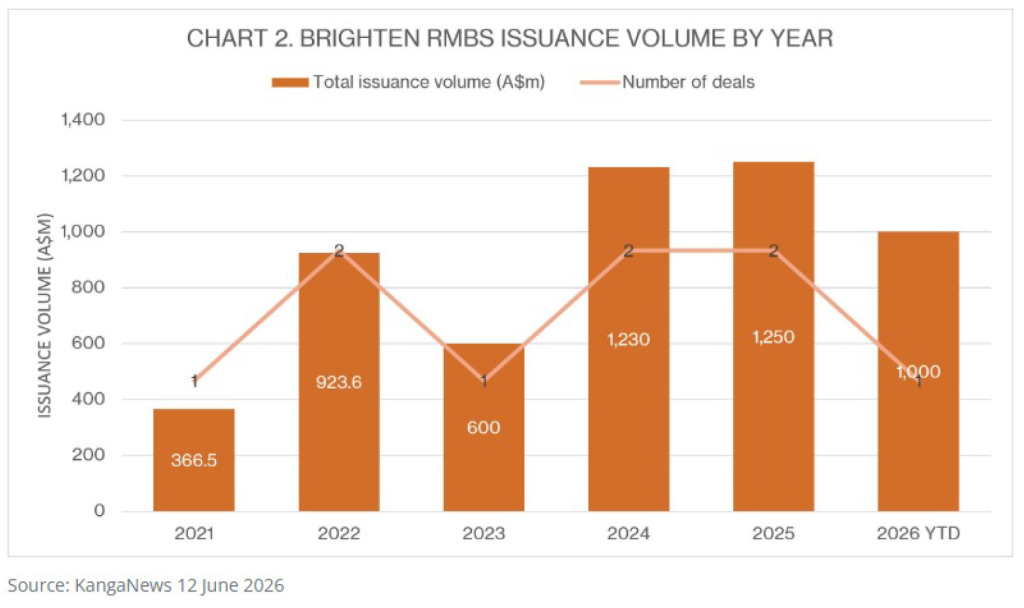

Frearson says the key benefit of the deal was funding diversification and the addition of longer-term financing to Brighten’s toolkit, though RMBS issuance (see chart) will remain the primary funding channel.

“The bullet structure provides longer-term funding and remains fully invested throughout its life. Unlike an RMBS transaction, which gradually pays down, the portfolio is replenished with new Brighten originations as loans repay,” Frearson adds

He highlights benefits for investors including Brighten’s strong origination expertise and track record. He points to the lender’s 90-day arrears rate of 0.33 per cent -which he says is below the industry average as well as the secured nature of the notes and the 3 per cent credit enhancement provided by RAM

Investors in the OTC notes will receive a fixed-rate coupon of 6.9 per cent. This compares with the ASX listed notes’ floating-rate coupon of bank bills plus 300 basis points, equivalent to around 7.3 per cent at current market levels.

For investors, there was also a likely pricing incentive compared with the mezzanine tranches of a securitisation deal.

“The closest comparison is the triple-B component of a mezzanine RMBS tranche, which is currently pricing at around 180-190 basis points over bills, “Frearson explains. “The RAM income capital notes priced at 242 basis points over, offering a yield pickup for investors willing to undertake the credit analysis.”

He continues: “Another benefit is the available volume. Mezzanine RMBS allocations are often limited because they represent a small part of the capital structure. In this case, the entire transaction was available at that spread level.”

FUTURES

RAM anticipates that it will become a repeat issuer across the listed and OTC markets as it grows its programme in step with Brighten’s loan book.

“Ideally, we’d like to tap the current note or complete another transaction next year,” Frearson notes

He expects the next senior notes issuance will likely be larger, potentially A$150 million or more, supported by greater investor engagement prior to the deal and longer execution timeframe.

“This was our first OTC transaction and we did not have the opportunity to engage fully with investors given the pricing constraints and robust day-one demand. We are confident that next time we can increase demand and grow the size of the offering by broadening investor engagement.”

Even so, RMBS and warehousing will remain the core components of Brighten’s overall funding mix. Frearson comments: “At the moment, the notes account for a little more than 5 per cent of the Brighten loan book. We would expect the notes to grow broadly in line with the Brighten loan book over time, remaining around the 3-5 per cent range.”